The COVID-Compliant Way to Refinance or Purchase a New Home

With all that is taking place around us, purchasing a home may not be top-of-mind for most people.

But then again, maybe it is. Before this crisis hit, the spring home buying season was just getting started. And the reality is, many families do need to sell and buy homes, even during a pandemic.

Once the crisis passes, there will be even more buyers and sellers. Some mortgage forecasters are predicting a pent-up demand of buyers flooding the market.

Once the crisis passes, there will be even more buyers and sellers. Some mortgage forecasters are predicting a pent-up demand of buyers flooding the market.

If you anticipate house shopping once the all-clear is given and social distancing rules are eased, now is the time to get ready.

Those who are pre-approved will be in a better position to have their offers accepted once the real estate market gets back into full or partial stride.

Another way home owners are taking advantage is by refinancing. Mortgage rates are still historically low. Many consumers are enjoying big savings by refinancing.

Many of you might be thinking, “how can I get a mortgage with social distancing rules in place and me stuck at home?”

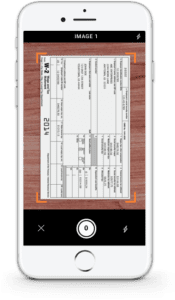

The answer is: with the Home Snap mobile app from Michigan Mortgage.

Even in normal times, Home Snap offers convenience for getting a new home loan or refinancing. The app lets you do everything from the convenience of your home. The app lets you get pre-approved, view your progress, securely upload documents, digitally sign documents, and easily message your loan officer.

In these restricted times, Home SNAP is a necessity. Like workers at many companies, Michigan Mortgage loan officers are working from home for the time being. But that doesn’t mean the mortgage services we provide have stopped.

Using Home Snap, you can:

- Start the Application Process

- Calculate Payments Easily

- Securely Scan and Upload Documents From Your Phone

- Digitally Sign Documents

- Message Your Loan Officer and Realtor Instantly

- See Your Progress

- Get Updates as You Go

With mortgage rates at record lows, many homeowners are taking advantage by refinancing their existing mortgages. Home Snap is ideal for these homeowners as well.

“We have many customers who are using Home Snap to refinance safely and securely while they are sitting at home, all without having to meet face-to-face. Customers love the convenience and safety, as well as the great rates.”says Mortgage 1 CEO Mark Workens.

In pre-coronavirus times, hundreds of Michigan Mortgage customers took advantage of Home Snap to get a new mortgage or to refinance. You can, too. To get started, visit the Home Snap page on our website.

This blog post originally appeared on mortgageone.com. Michigan Mortgage is a DBA of Mortgage 1.

It is important for you to analyze your spending habits. If you do not have a budget, you should start one now. This will help you understand you spending habits so that the lifestyle that is important to you will be maintainable as a homeowner.

It is important for you to analyze your spending habits. If you do not have a budget, you should start one now. This will help you understand you spending habits so that the lifestyle that is important to you will be maintainable as a homeowner.

So, what is the best use of those funds? Like most questions, the answers vary depending on the individual situation. If you are swimming in debt it may be time to pay some of that debt off. If you have not funded your 401(k) for the year, perhaps that money is best used to invest in a tax deferred plan.

So, what is the best use of those funds? Like most questions, the answers vary depending on the individual situation. If you are swimming in debt it may be time to pay some of that debt off. If you have not funded your 401(k) for the year, perhaps that money is best used to invest in a tax deferred plan.

Home Snap at a glance:

Home Snap at a glance:

Home Snap at a glance:

Home Snap at a glance:

Home Equity at All-Time High

Home Equity at All-Time High

However, for many lenders, that’s not enough to be considered a good mortgage candidate. As a borrower, your DTI is utilized in various situations to determine your level of risk. For instance, if your DTI is too high, opportunities to make a big purchase, such as a mortgage, may be limited.

However, for many lenders, that’s not enough to be considered a good mortgage candidate. As a borrower, your DTI is utilized in various situations to determine your level of risk. For instance, if your DTI is too high, opportunities to make a big purchase, such as a mortgage, may be limited.

Appraisals are required as past of the home-buying process. Home inspections are not, but they may be one of the most beneficial things you can do for your financial future. A home inspection will ensure that you don’t buy a money pit.

Appraisals are required as past of the home-buying process. Home inspections are not, but they may be one of the most beneficial things you can do for your financial future. A home inspection will ensure that you don’t buy a money pit.